Japan: companies navigating demographic shifts

Trip report – October 2024

Long lifespans and a birthrate that fell below the 2.1 replacement rate 50 years1 ago and is currently at a rate of 1.3, guarantees pensioners will increasingly dominate Japanese society over the coming century.

Although surrounding nations like South Korea and Taiwan follow closely behind, Japan is the first major economy to enter this demographic phase, leaving policymakers the unenviable task of facing down its challenges without a roadmap to follow. Tokyo’s childless train cars and construction sites staffed by greying labourers are the visible tip of a demographic iceberg that is destined to get worse.

Thankfully, we invest our client’s capital in companies and not countries and we are free to avoid companies significantly impacted by challenging demographic trends, even if they are included in the benchmark. Instead of focusing on Japan's stars of yesterday, which increasingly face shrinking markets, we invest in Japanese companies that we believe have their best days ahead. Typically, this means they are addressing Japan’s growing productivity issues or taking high-quality Japanese products into overseas markets. Below are two companies we met during our trip to Japan in June that we believe provide such solutions.

MonotaRO – growth of stock items and customers 2010 - 20235

For MonotaRO, the key barrier to growth is convincing older factory managers set in their ways to adopt this new technology. Here, demographics are on their side. Every year, thousands of older factory managers retire and are replaced by younger colleagues more willing to use the company’s technology.

Anest Iwata - taking Japanese products overseas

A trait we admire in Japanese businesses is that delighting customers and building high quality products almost always comes first. Despite this, Japanese companies can often lack the commercial awareness to take these world class products overseas and charge prices that reflect the quality of what they provide. But creating world class products is the hard part! All it takes for these companies to realise their potential is the introduction of a commercially focussed leader.

Anest Iwata is a company we believe is on this trajectory. Founded by the Iwata brothers in the 1920’s, the business initially made spray guns for painting and then expanded into manufacturing the air compressors needed to power them. The company is now a world class manufacturer of oil-free air compressors, and as we know from other global air compressor companies such as Sweden’s Atlas Copco, this is a very profitable business to be in if managed well. Until recently though, Anest Iwata was run with a domestic focus and without much regard to increasing profitability or returns. It had great products but lacked ambition to grow in the profitable global market. The chart below6 shows the difference in operating margin (how much profit a company makes on sales after paying for production costs) between the two companies.

Operating margin

A focus on overseas growth and profitability has come recently with the appointment of a new CEO, Shinichi Fukase, in 2022. He has prioritised growing the business outside of Japan and has shown a willingness to make the tough choices and up-front investments required to achieve this. We have been particularly impressed by the difficult decision made this year to raise prices in the domestic market, which has been delivering low profit margins. This is a strong signal of a mindset change within the company, and we look forward to seeing it progress.

No sweeping country-level story of demographic gloom will ever be sufficient to describe this huge and varied market. With businesses like MonotaRO and Anest Iwata we remain confident by the investment opportunities in Japan.

Risk factors

Capital at risk. The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested.

How to invest

There are different ways to buy shares in an investment trust.

MonotaRO - improving productivity

MonotarRO is a one stop online shop for products including nuts, bolts and bearings that keep factories running. By making factories more efficient they play an important role in making Japan more productive. Today, the vast majority of these factory products in Japan are still ordered by a manager thumbing through a thick catalogue and calling up a distributor. In a labour scarce economy, the time spent every day searching through a thick book for niche products is a significant cost and so too is the idle time spent waiting for products to arrive when local distributors do not have them in stock.

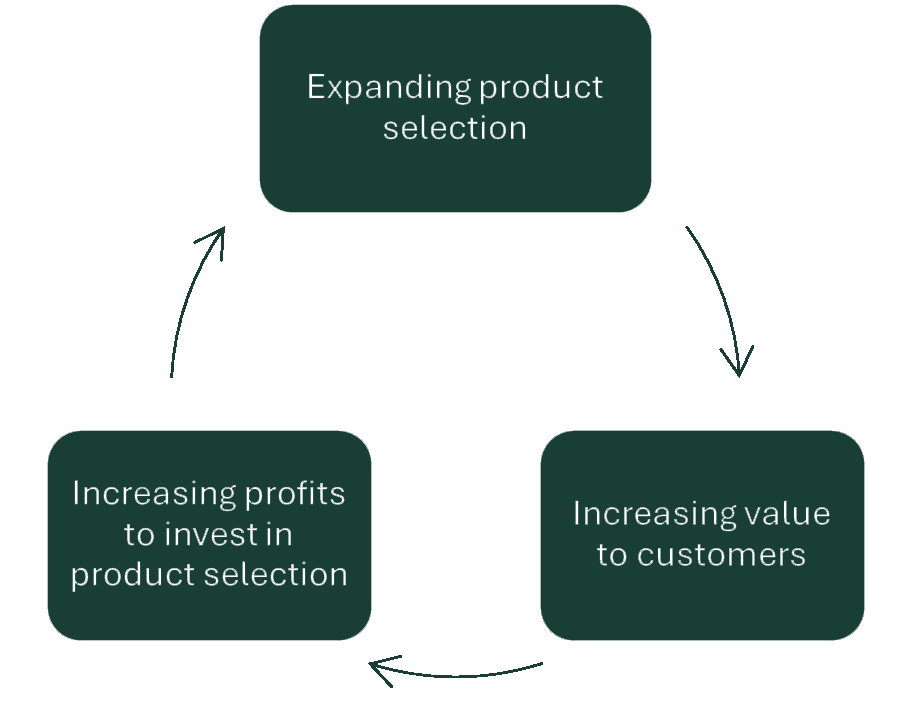

Their solution is simple. An online shop with a wider and deeper number of stock items that reduce searching and waiting time. Since we first met the company in 2013, customers have increased tenfold and profits are up over 700%.3 At the core of this success is a positive feedback loop that has continually increased their value to customers:

MonotaRO positive feedback loop

Most factories will never order the 20 millionth product on their website, but your factory production line might shut down without its timely replacement. Local distributors do not sell enough of this product to justify keeping it in stock, but MonotaRO, selling to over 10 million customers4, can keep it in stock and deliver it to you within 24 hours. This value proposition is so compelling that customers rarely leave MonotarRO.

Risk factors

This web page is a financial promotion for Pacific Assets Trust plc (the “Trust”) only for those people resident in the UK and Ireland for tax and investment purposes.

Investing involves certain risks including:

- The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested.

- Emerging market risk: emerging markets tend to be more sensitive to economic and political conditions than developed markets. Other factors include greater liquidity risk, restrictions on investment or transfer of assets, failed/delayed settlement and difficulties valuing securities.

- Specific region risk: investing in a specific region may be riskier than investing in a number of different countries or regions. Investing in a larger number of countries or regions helps spread risk.

- Currency risk: the Trust invests in assets which are denominated in other currencies; changes in exchange rates will affect the value of the Trust and could create losses. Currency control decisions made by governments could affect the value of the Trust’s investments.

- The Trust’s share price may not fully reflect net asset value.

Where featured, specific securities or companies are intended as an illustration of investment strategy only, and should not be construed as investment advice or a recommendation to buy or sell any security.

For an overview of the terms of investment, risks, returns, costs and charges please refer to the Key Information Document.

If you are in any doubt as to the suitability of the Trust for your investment needs, please seek investment advice.

Important information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should conduct your own due diligence and consider your individual investment needs, objectives and financial situation and read the relevant offering documents for details including the risk factors disclosure.

Any person who acts upon, or changes their investment position in reliance on, the information contained in these materials does so entirely at their own risk.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

Past performance is not indicative of future performance. All investment involves risks and the value of investments and the income from them may go down as well as up and you may not get back your original investment. Actual outcomes or results may differ materially from those discussed. Readers must not place undue reliance on forward-looking statements as there is no certainty that conditions current at the time of publication will continue.

References to specific securities (if any) are included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. Any securities referenced may or may not form part of the holdings of First Sentier Investors' portfolios at a certain point in time, and the holdings may change over time.

References to comparative benchmarks or indices (if any) are for illustrative and comparison purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, and have limitations when used for comparison or other purposes because they may have volatility, credit, or other material characteristics (such as number and types of securities) that are different from the funds managed by First Sentier Investors.

Selling restrictions

Not all First Sentier Investors products are available in all jurisdictions.

This material is neither directed at nor intended to be accessed by persons resident in, or citizens of any country, or types or categories of individual where to allow such access would be unlawful or where it would require any registration, filing, application for any licence or approval or other steps to be taken by First Sentier Investors in order to comply with local laws or regulatory requirements in such country.

This material is intended for ‘professional clients’ (as defined by the UK Financial Conduct Authority, or under MiFID II), ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) or Financial Markets Conduct Act 2013 (New Zealand) and ‘professional’ and ‘institutional’ investors as may be defined in the jurisdiction in which the material is received, including Hong Kong, Singapore, Japan, and the United States, and should not be relied upon by or be passed to other persons.

The First Sentier Investors funds referenced in these materials are not registered for sale in the United States and this document is not an offer for sale of funds to US persons (as such term is used in Regulation S promulgated under the 1933 Act). Fund-specific information has been provided to illustrate First Sentier Investors’ expertise in the strategy. Differences between fund-specific constraints or fees and those of a similarly managed mandate would affect performance results.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group (MUFG). Certain of our investment teams operate under the trading names AlbaCore Capital Group, FSSA Investment Managers, Stewart Investors and RQI Investors all of which are part of the First Sentier Investors group.

This material may not be copied or reproduced in whole or in part, and in any form or by any means circulated without the prior written consent of First Sentier Investors.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Australia and New Zealand by First Sentier Investors (Australia) IM Ltd, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

- European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in

- Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Investors, FSSA Investment Managers, Stewart Investors, RQI Investors and Igneo Infrastructure Partners are the business names of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this advertisement or material has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B), FSSA Investment Managers (registration number 53314080C), Stewart Investors (registration number 53310114W), RQI Investors (registration number 53472532E) and Igneo Infrastructure Partners (registration number 53447928J) are the business divisions of First Sentier Investors (Singapore).

- United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

- United States by First Sentier Investors (US) LLC, authorised and regulated by the Securities Exchange Commission (RIA 801-93167).

- other jurisdictions, where this document may lawfully be issued, by First Sentier Investors International IM Limited, authorised and regulated in the UK by the Financial Conduct Authority (FCA ref no. 122512; Registered office: 23 St. Andrew Square, Edinburgh, EH2 1BB; Company no. SC079063).

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group