Quarterly Trust update

Pacific Assets Trust quarterly update - Q1 2025

Significant Trust changes

Broad market indices in the Asia Pacific region moved slightly lower in sterling terms over the first quarter of 2025. Perhaps of greater significance was that political turbulence resulted in a wide divergence of returns on a country level. Market indices in China, South Korea and Singapore moved higher but fell across the rest of the region, with some markets suffering double-digit falls.

Most notable was the extent of the divergence in returns between markets in India (down) and China (up). Investors’ enthusiasm for Chinese equities came in response to DeepSeek’s impressive demonstration of the progress the country is making in AI, some market-friendly rhetoric from the government in Beijing and hopes that the United States’ trade tariffs might not prove too onerous. In contrast, while there was relatively little news from India, share prices there fell back from elevated levels, as they did in many other parts of the world; returns from the Indian market over the quarter were broadly in-line with those from markets in the United States.

During the quarter, and on behalf of the Trust, we added new positions in S.F. Holding (China: Industrials), Mindray (China: Health Care) and Alibaba (China: Consumer Discretionary). S.F. Holding is China’s number one provider of logistics and is well placed to benefit from the growth in time-sensitive logistics across Asia. Mindray is a global leader in affordable medical devices and is steadily climbing up the value chain. Alibaba, meanwhile, has an important part to play amid China’s new emphasis on increasing national self-reliance, particularly in the realms of AI and cloud computing. In recent years, the stewards of Chinese companies have, often for the first time, been tested by genuine economic and political adversity. They have applied the lessons learned, strengthening their franchises and balance sheets. This, in combination with valuations that appear modest by global standards, means we have been identifying a greater number of new investment ideas in China.

Elsewhere, we established new positions in Bank of the Philippine Islands (Philippines: Financials) and BDO Unibank (Philippines: Financials). Both are family owned and professionally managed. In India, we took advantage of recent weakness to add a new holding in Bajaj Auto (India: Consumer Discretionary), a leading manufacturer of motorcycles, scooters and auto rickshaws backed by a high-quality steward.

Lower valuations also prompted us to build the Trust’s positions in two companies which we first purchased last year. Bajaj Holdings & Investment (India: Financials) is a holding company with auto and finance businesses and Sundaram Finance (India: Financials) provides vehicle finance, home loans and general insurance.

We sold the entirety of the Trust’s holding in Tata Consumer Products (India: Consumer Staples) on valuation grounds. We also sold out of Syngene (India: Health Care), Dr. Reddy’s Laboratories (India: Health Care) and Cyient (India: Information Technology) because of their vulnerability to policy changes from the White House. Finally, we sold ICICI Lombard (India: Financials), IndiaMART (India: Industrials) and Koh Young Technology (South Korea: Information Technology). These were small positions and we had better ideas elsewhere.

We continued to reduce the holding in TSMC (Taiwan: Information Technology) as evidence continued to mount that it is losing control of capital expenditure. To control position sizes, we reduced Mahindra & Mahindra (India: Consumer Discretionary), and CG Power (India: Industrials).

As the long period of US exceptionalism draws to an end, we hope investors will begin to pay attention to the abundance of attractively valued companies to be found in the Asia Pacific region. Clearly, if the US economy falters and global demand falls, then economies across Asia will be impacted, albeit to differing degrees. We are also conscious that political risks appear to be rising in many Asian countries. Those risks, however, are far from uniform. The region’s technology complex, centred around Taiwan, South Korea and China, would appear to be particularly vulnerable to a global slowdown. India, by contrast, remains a domestically driven growth story and, as such, is somewhat isolated from the tumult in the global economy. The Philippines, meanwhile, could receive a significant economic boost if a global slowdown results in a meaningful fall in oil prices.

Predicting how any of today’s economic and geopolitical challenges will play out lies beyond our remit and our skillset. Fortunately, many of the Asian companies held in the Trust have long memories; they still have the scar tissue formed during previous crises. These businesses have been forced to learn, to adapt and to become resilient. As a result, we believe they are set up not only to perform when conditions are fair but to navigate through whatever political and economic turbulence lies ahead.

Risk factors

Capital at risk. The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested.

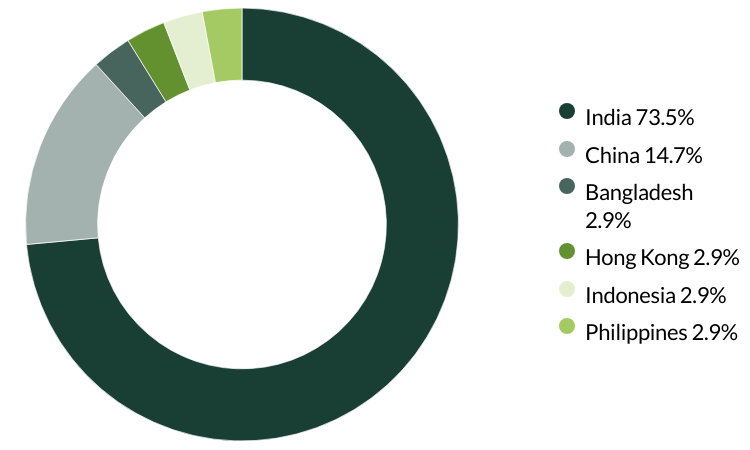

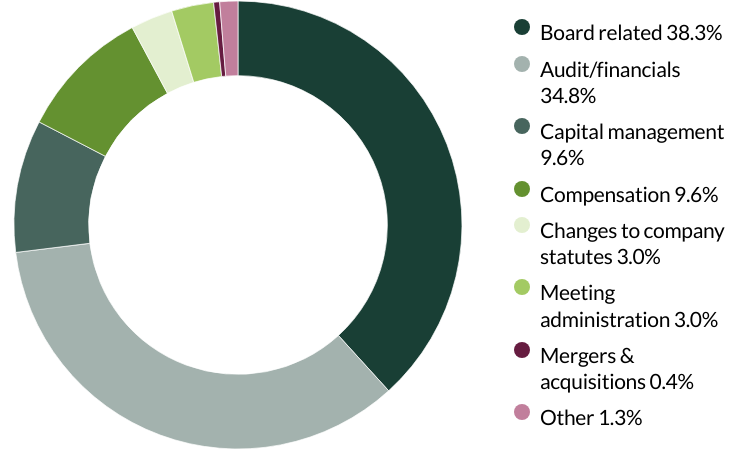

Proxy voting: 1 January - 31 March 2025

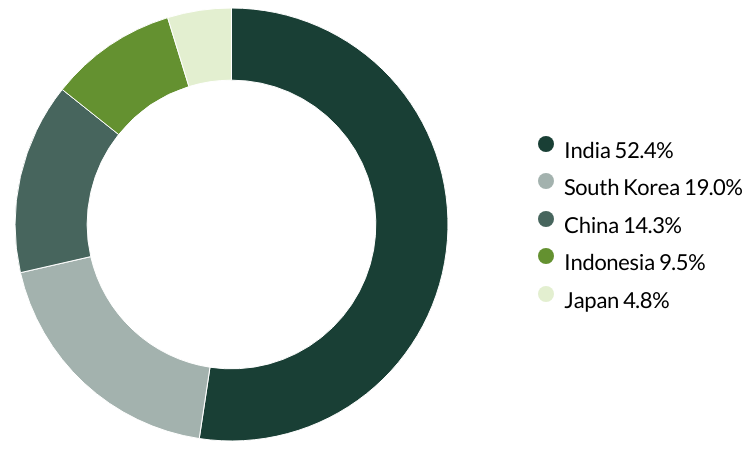

Proxy voting by country of origin

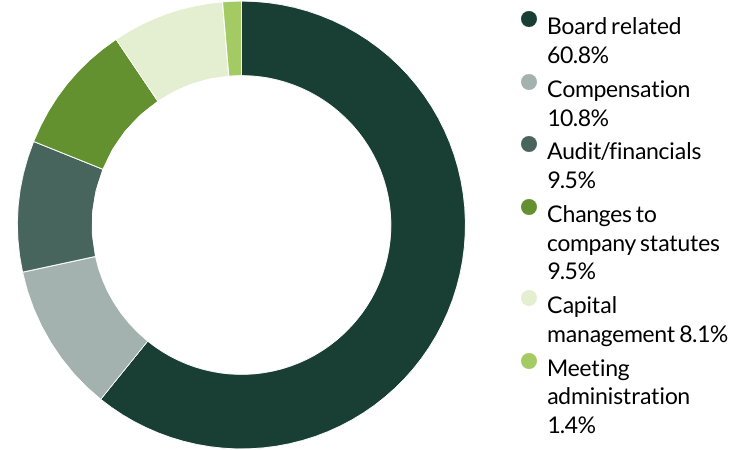

Proxy voting by proposal categories

During the quarter there were 74 resolutions from 20 companies to vote on. On behalf of the Trust, we voted against five resolutions.

We voted against the election of a director and their remuneration at IndiaMART as we seek to encourage greater diversity and independence on the board. (one resolution)

We voted against the election of two directors and an audit committee member at Samsung Electronics as we do not believe them to be truly independent. (three resolutions)

We voted against the election of the audit committee chair at Unicharm as we do not believe they are independent. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Download a PDF copy

Select Strategy update and/or Proxy voting to produce a report. You can then download a copy of the report by clicking on the button.

Previous Quarterly Shareholder updates:

Q4: 1 October - 31 December 2024

Significant Trust changes

Over most three-month periods, there should be relatively little change in the Trust portfolio. We aim to build resilient portfolios of high-quality companies with diversified streams of cash flows that have the ability to grow in value over the long term.

Chinese equities gave back some gains from the dramatic autumn stimulus which challenged comparative performance in the third quarter of 2024. The performance of the Indian market index struggled after some of the largest companies in India faced governance issues that became subject to enquiry by the regulator in the United States. The re-election of Mr Trump also seemed to distract global investors from Asian equities. At Stewart Investors we continue to concentrate on bottom-up stock selection rather than overly focus on unpredictable macro news flow.

On behalf of the Trust, we purchased DFI Retail Group (Hong Kong: Consumer Staples), a pan-Asian retailer stewarded by the Keswick family and MANI (Japan: Health Care), a Japanese medical device company. We also bought Naver (South Korea: Communication Services), South Korea’s dominant internet search engine which has significantly improved its capital allocation in recent years.

During the quarter we took advantage of attractive valuations to add to the Trust’s positions in AirTAC International (Taiwan: Industrials) and Yiheda Automation (China: Industrials).

Due to waning conviction, high valuations, or finding better ideas elsewhere, we sold Pentamaster (Malaysia: Information Technology), Advanced Energy Solution (Taiwan: Industrials) and Samsung C&T (South Korea: Industrials).

To control position sizes, we trimmed Mahindra & Mahindra (India: Consumer Discretionary), CG Power (India: Industrials), Marico (India: Consumer Staples), TSMC (Taiwan: Information Technology), Unicharm (Japan: Consumer Staples), Dr. Lal PathLabs (India: Health Care) and Chroma ATE (Taiwan: Information Technology).

Views on investment opportunities in Asia have not changed; we continue to look to invest in high-quality companies that are aligned with sustainable development. We look for stewards who are low profile, competent, long-term decision makers, franchises free from political agendas and financials that are resilient, not frail. Our focus is on quality, and we remain indifferent to many of the large, well-known companies, regardless of lower valuations.

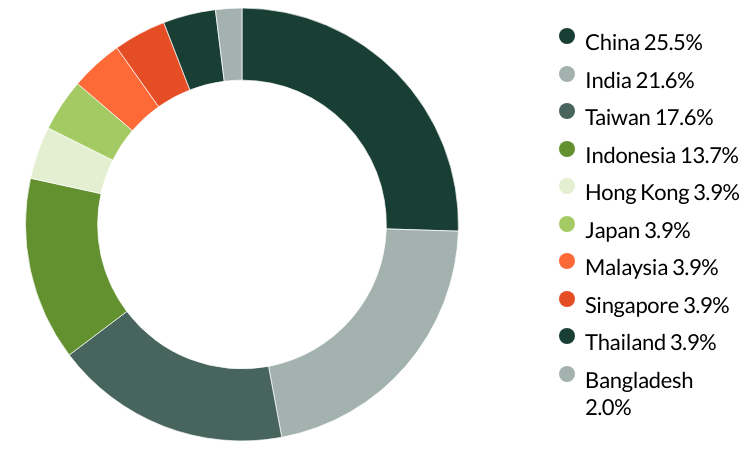

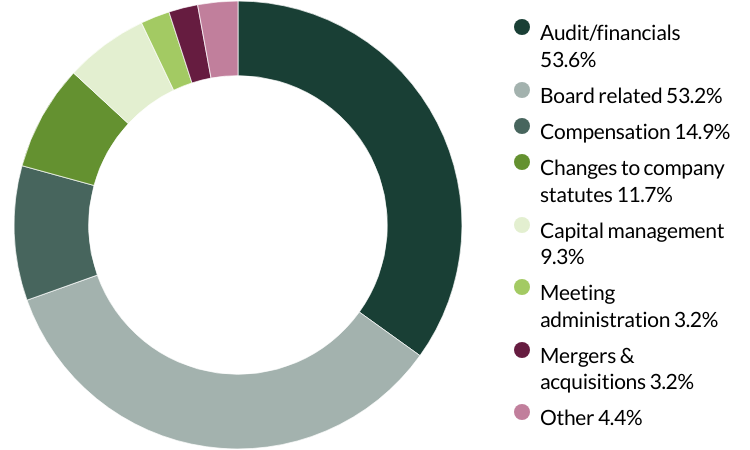

Proxy voting: 1 October - 31 December 2024

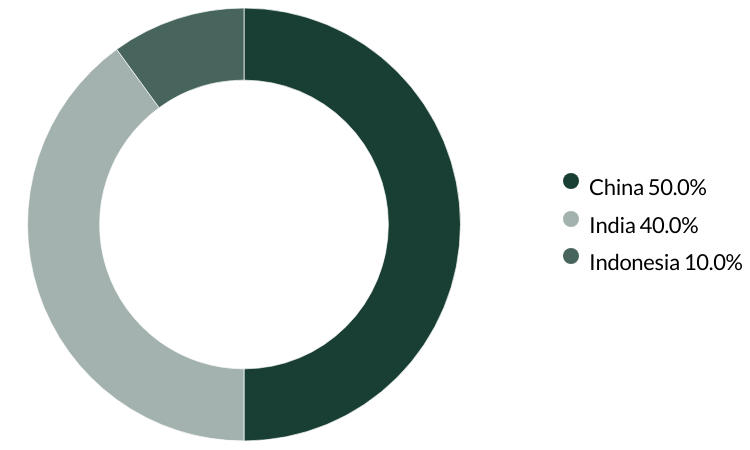

Proxy voting by country of origin

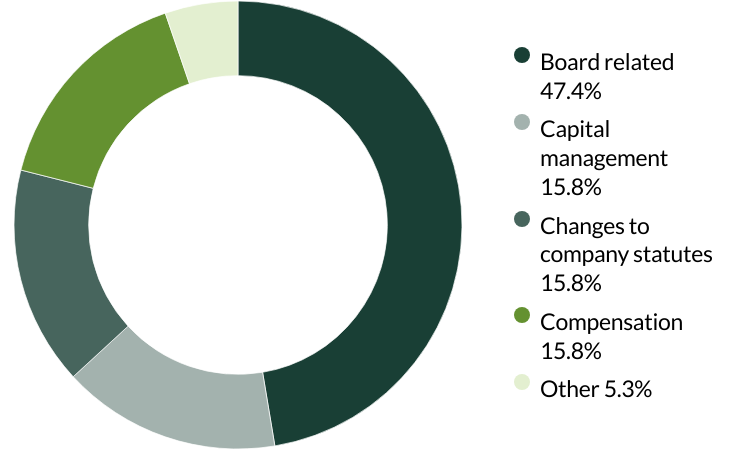

Proxy voting by proposal categories

During the quarter there were 19 resolutions from nine companies to vote on. On behalf of the Trust, we did not vote against any resolutions.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Q3: 1 July - 30 September 2024

Significant Trust changes

Over most three-month periods, there should be relatively little change in the Trust portfolio. We aim to build resilient portfolios of high-quality companies with diversified streams of cash flows that have the ability to grow in value over the long term.

During the last few days of the quarter the Chinese central bank and government announced monetary and fiscal stimulus measures for the economy, causing Chinese stocks to rally significantly. Whilst it is heartening to see the Chinese authorities attempting to address the issues within the economy it remains unclear whether this stimulus will adequately address structural issues like the lack of consumer demand.

The Trust bought Ayala (Philippines: Industrials), a 190-year-old Filipino conglomerate stewarded by the Ayala family who in recent years have appointed the first ever non-family CEO. It also purchased Yiheda Automation (China: Industrials), China’s leading supplier of factory automation components, which has the opportunity to consolidate a growing, largely informal market. Finally, the Trust bought Blue Dart Express (India: Industrials), a logistics provider focussed on express parcel deliveries and majority-owned by DHL Group.

During the quarter we continued to add to Techtronic Industries (Hong Kong: Industrials) and increased the position in Tata Communications (India: Communication Services).

We controlled the position size of the Trust’s large holdings in Mahindra & Mahindra (India: Consumer Discretionary), CG Power (India: Industrials), and Cholamandalam Financial Holdings (India: Financials). The Trust also trimmed positions in HDFC Bank (India: Financials), Aavas Financiers (India: Financials), Hoya (Japan: Health Care), and Unicharm (Japan: Consumer Staples).

On behalf of the Trust we sold RBL Bank (India: Financials) and Unilever Indonesia (Indonesia: Consumer Staples), both of which were smaller positions that we struggled to build conviction in.

Views on investment opportunities in Asia have not changed; the strategy continues to look to invest in high-quality companies that are aligned with sustainable development. We look for stewards who are low profile, competent, long-term decision makers, franchises free from political agendas and financials that are resilient, not frail. Our focus is on quality, and we remain indifferent to many of the large, well-known companies, regardless of lower valuations.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Proxy voting: 1 July - 30 September 2024

Proxy voting by country of origin

Proxy voting by proposal categories

During the quarter there were 230 resolutions from 30 companies to vote on. On behalf of the Trust, we voted against four resolutions.

We voted against the appointment of the auditor at Philippine Seven as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. We also voted against proposals on transaction of business, as the company did not provide enough information about the proposals. We wanted to avoid giving them unrestricted decision-making power without sufficient clarity. (two resolutions)

We voted against the appointment of the auditor at Shanthi Gears as the company did not disclose the name of the proposed auditor. (one resolution)

We voted against the appointment of the auditor at Vitasoy as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Q2: 1 April - 30 June 2024

Significant Trust changes

Over most three-month periods, there should be relatively little change in the Trust portfolio. We aim to build resilient portfolios of high-quality companies with diversified streams of cash flows that have the ability to grow in value over the long term.

During the quarter we initiated a new position in ESAB India (India: Industrials). The company is the market leader within India for welding equipment and consumables. It is a subsidiary of ESAB (chaired by Mitch Rales, the founder of Danaher) and stands to benefit from manufacturing moving out of China and into India.

We exited Telkom Indonesia (Indonesia: Communication Services), Kingmed Diagnostics (China: Health Care), Amoy Diagnostics (China, Health Care), WuXi Biologics (China: Health Care), and Kotak Mahindra Bank (India: Financials).

We sold WuXi Biologics after a proposed bill in the United States Congress aimed to restrict some Chinese biotech business tie-ups with United States companies due to national security concerns. It was a mistake to invest in WuXi Biologics given the geopolitical risk the company is exposed to.

We sold Amoy Diagnostics and Kingmed Diagnostics due to their exposure to regulatory risk. Despite the value provided to customers it is difficult for us to assess the risk of forced pricing cuts as the government drives to reduce healthcare spending. This quarter, we also exited DBH Finance (Bangladesh: Financials) from the portfolio. Although quality remains intact on a bottom-up basis, the company faced increased regulatory pressures across the sector and deteriorating macro-economic conditions.

We took advantage of a lower valuations to build our positions in Shenzhen Inovance (China: Industrials) and Techtronic Industries (Hong Kong: Industrials). We also added to Samsung C&T (South Korea, Industrials), Samsung Biologics (South Korea: Health Care), and Info Edge (India: Communication Services).

To finance new investments and latest additions, and to control position size we trimmed holdings in Tech Mahindra (India: Information Technology), Mahindra & Mahindra (India: Consumer Discretionary), and CG Power (India: Industrial).

Views on investment opportunities in Asia have not changed; we continue to look to invest in high-quality companies that are aligned with sustainable development. We look for stewards who are low profile, competent, long-term decision makers, franchises free from political agendas and financials that are resilient, not frail. Our focus is on quality, and we remain indifferent to many of the large, well-known companies, regardless of lower valuations.

Proxy voting: 1 April - 30 June 2024

Proxy voting by country of origin

Proxy voting by proposal categories

During the quarter there were 381 resolutions from 44 companies to vote on. On behalf of the Trust, we voted against 12 resolutions.

We abstained from voting on amendments to work systems for independent directors and board meeting procedures at Amoy Diagnostics as the company did not provide sufficient data on the proposed amendments. (two resolutions)

We voted against the appointment of the auditor at Glodon, Sheng Siong, Unilever Indonesia, ViTrox, Yifeng Pharmacy Chain and Zhejiang Supor as they have been in place for over 10 years and the companies’ have given no information on intended rotation. We believe rotating an auditor on a relatively frequent basis (e.g. every 5-10 years) helps to ensure a fresh pair of eyes are examining the accounts, and follows best practice. (six resolutions)

We voted against proposals regarding transaction of business at Humanica Public and Kasikornbank as the companies provided insufficient detail on the proposals and we wish to avoid unfettered discretion. (two resolutions)

We voted against the proposed employee stock ownership plan at Midea as we believe non-executive director involvement could lead to conflict of interest and would not be in shareholders' interest. (three resolutions)

We voted against a proposal regarding capital management at Pentamaster as we do not believe shares should be issued without pre-emptive rights. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Risk factors

This web page is a financial promotion for Pacific Assets Trust plc (the “Trust”) only for those people resident in the UK and Ireland for tax and investment purposes.

Investing involves certain risks including:

- The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested.

- Emerging market risk: emerging markets tend to be more sensitive to economic and political conditions than developed markets. Other factors include greater liquidity risk, restrictions on investment or transfer of assets, failed/delayed settlement and difficulties valuing securities.

- Specific region risk: investing in a specific region may be riskier than investing in a number of different countries or regions. Investing in a larger number of countries or regions helps spread risk.

- Currency risk: the Trust invests in assets which are denominated in other currencies; changes in exchange rates will affect the value of the Trust and could create losses. Currency control decisions made by governments could affect the value of the Trust’s investments.

- The Trust’s share price may not fully reflect net asset value.

Where featured, specific securities or companies are intended as an illustration of investment strategy only, and should not be construed as investment advice or a recommendation to buy or sell any security.

For an overview of the terms of investment, risks, returns, costs and charges please refer to the Key Information Document.

If you are in any doubt as to the suitability of the Trust for your investment needs, please seek investment advice.